STATE TRUST FUNDS INTENDED FOR CLEANING UP DRY CLEANER SITES HAVE BEEN GREAT TO RELY ON. HOWEVER, MANY HAVE FALLEN ON HARD TIMES.

BY: DRU CARLISLE

Some Funds are either running out of money or have already sunset. What is the dry cleaning industry turning to for the money needed to respond to environmental liability? Dry cleaners are increasingly using their historical insurance policies to pay for environmental cleanup claims—protecting their business from financial ruin or bankruptcy.

The dry cleaning industry has seen more than its fair share of costly and complicated environmental contamination issues. In the past, eligible dry cleaners in almost 25% of the United States have been able to use money from state trust funds that were established solely for this purpose. Unfortunately, these state trust funds have proven to be not sustainable in most situations, and the number of available funds is declining. In the coming years, it’s anticipated that those looking to the state fund programs will experience even more delays in reimbursement of money already spent out-of-pocket, and or will lose the fund altogether.

Who is potentially impacted by this news? Any dry cleaner in Alabama, Connecticut, Illinois, Florida, Kansas, Missouri, North Carolina, Oregon, South Carolina, Tennessee, Texas, or Wisconsin.

This is frightening news for dry cleaners in these states, who are liable for cleaning up environmental contamination caused by cleaning solvents like PCE (Perc) or TCE. However, another financial solution is still available to dry cleaners—their historical Commercial General Liability (CGL) insurance policies. By finding their historical insurance policies, dry cleaners can use them as assets to help pay for their environmental investigation and cleanup. Those residing in states without trust funds have been doing it for years.

HOW CAN DRY CLEANERS USE HISTORICAL INSURANCE POLICIES TO PAY FOR ENVIRONMENTAL CLEANUPS?

Historical insurance policies are valuable assets that you can use to get money to pay for resolving environmental issues.

Commercial general liability (CGL) policies provide coverage to businesses for bodily injury, personal and property damage caused the business’ operations, products, or injury that occurs on the business’ premises. Most every business has old CGL policies since they are commonly purchased as a necessity to cover potential costs incurred by defending and reasonably resolving suits seeking to hold them liable for alleged bodily injuries or property damage.

Historical Commercial General Liability (CGL) policies from before 1985-86 typically don’t have a clause that disallows coverage for releases of contaminants. This means that if a dry cleaner can find their or their predecessor’s old insurance assets, then those policies can pay for the environmental investigation and cleanup required by the state’s environmental regulatory agency. Additionally, the policies would likely protect dry cleaners from any neighbors who decide to sue them for damage to their property. These policies also entitle dry cleaners to hire an environmental defense attorney at no charge and receive insurance payments immediately without upfront payments, unlike most state trust funds.

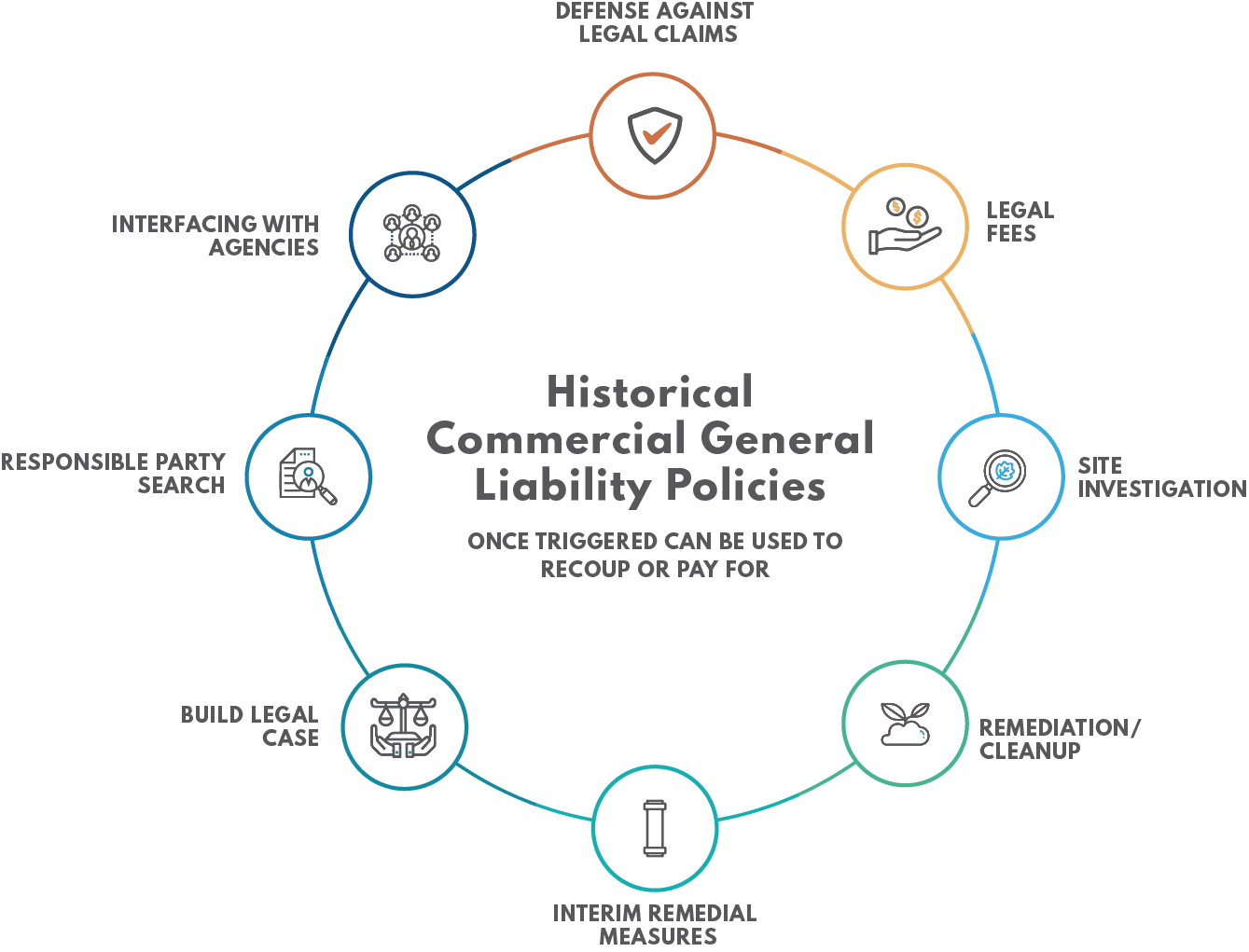

Once triggered historical commercial general liability (CGL) policies can be used to recoup or pay for 1) site investigation, 2) remediation/cleanup, 3) interim remedial measures, 4) building a legal case, 5) responsible party search, 6) interfacing with agencies, 7) defense against legal claims, and 8) legal fees. To learn more about CGL policies, visit How Does It Work? CGL Policies and Insurance Archeology.

HOW DO YOU FIND OLD INSURANCE POLICIES?

Insurance archeologists conduct insurance archeology to find lost or misplaced liability insurance policies that can defend and indemnify policyholders against claims such as environmental property damage claims.

EnviroForensics® is the nation’s leader in finding and using historical insurance coverage. Our insurance archeology division, PolicyFind™, has decades of experience identifying and locating lost, mislaid, or destroyed liability insurance policies for policyholders.

First, insurance archeologists retrace the genealogy of historical insurance coverage to identify past owners and operators who may have contributed or caused personal injury or environmental damage.

Next, they use an extensive specimen policy library to help confirm terms and conditions, research data services, and physical file searches to follow leads and locate evidence of old insurance policies.

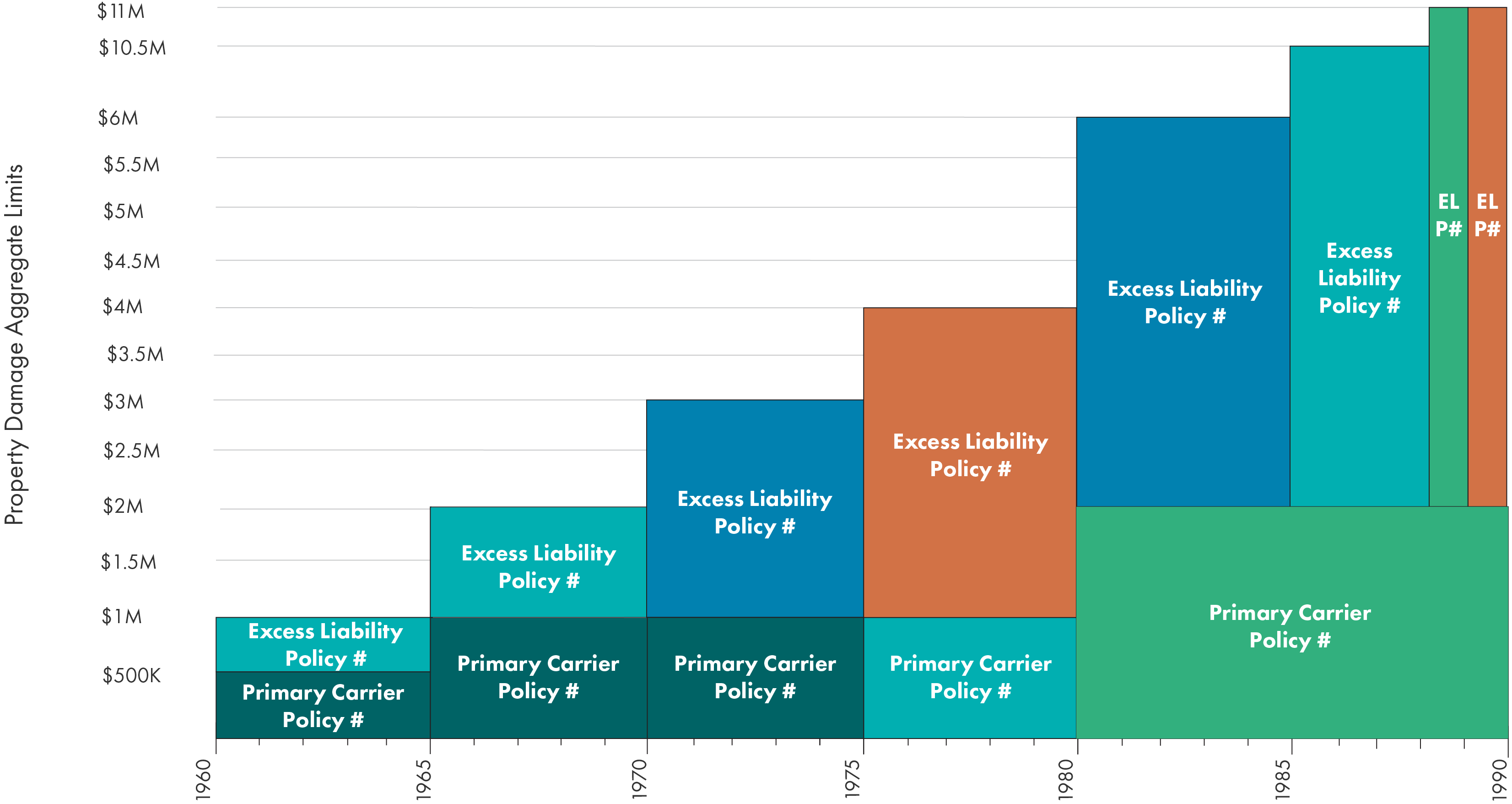

And finally, the results of the insurance archeology process are assembled into insurance coverage charts, which visually reconstruct the CGL insurance policies.

The rebuilding of historical land use and insurance can limit the liability of individual clients. Initiating coverage from these policies thereby creates an alternative funding source, which can protect a business from severe financial loss and even save a company from bankruptcy.

“If historical insurance policies are lost or misplaced, PolicyFind’s expert insurance archeologists will find the needed evidence of their existence and create a legally defensible historical insurance coverage chart—saving a dry cleaner’s livelihood,” says Jeff Carnahan, President of EnviroForensics.

Once identified and brought to light, the coverage provided by old insurance policies can be used to hire an environmental consulting firm with specialized expertise in serving the dry cleaning industry by cleaning up its historical environmental pollution problems.

HOW ENVIROFORENSICS CAN HELP

EnviroForensics® is the nation’s leading environmental engineering firm serving dry cleaners. EnviroForensics is the only full-service environmental firm that performs insurance archeology to locate money to pay for environmental investigation, cleanup, and legal fees. EnviroForensics helps clients get their cleanups paid for without significant cost to the clients or their businesses while restoring their property to fair market value.

To find out if historical insurance assets are an available funding avenue for you, contact us for a confidential consultation.

Dru Carlisle, Director of Drycleaner Accounts

Dru Carlisle, Director of Drycleaner Accounts

For over 10 years, Dru has helped numerous business and property owners facing regulatory action, navigate and manage their environmental liability. Dru has vast experience in assisting dry cleaners in securing funding for their environmental cleanups through historical insurance policies. Dru is a member of numerous drycleaning associations in addition to serving on the Midwest Drycleaning and Laundry Institute (MWDLI) advisory council and on the Drycleaning & Laundry Institute Board (DLI) as an Allied Trade District Committee Member.